Australian Dollar overtakes Sterling as the strongest one for the week, as supported by return of risk-mode markets. In particular, industrial metal is having strong rally with copper trading up 2% at the time of writing. Sterling shrugs off poor retail sales but was supported by PMI and upbeat comments from BoE official. Euro is also strong as boosted by strong manufacturing PMIs from Eurozone, Germany and France. On the other hand, Dollar is now experience heavy selloff.

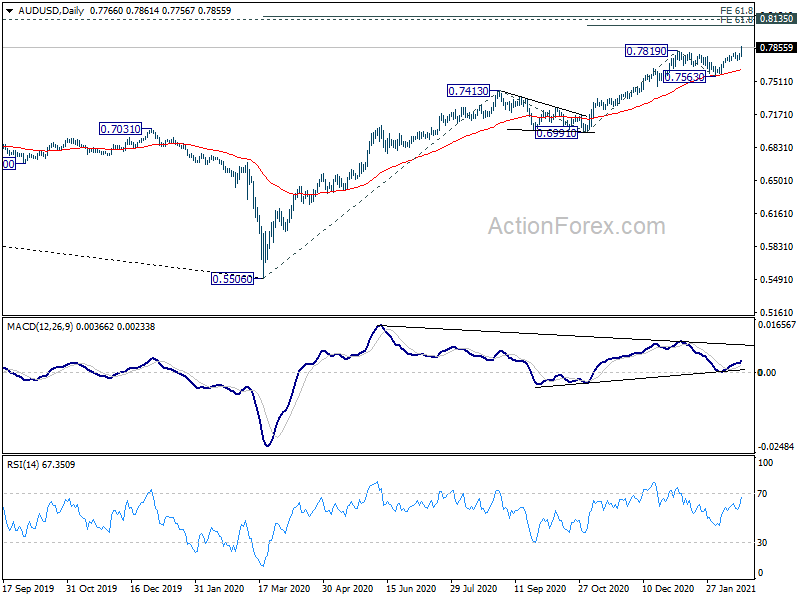

Technically, USD/CAD’s break of 1.2608 suggest resumption of fall from 1.2880 to 1.2588 low. Break will resume larger down trend from 1.4667. AUD/USD’s strong break of 0.7819 already confirms resumption of up trend from 0.5506. A question is whether EUR/USD would break through 1.2168 minor resistance, and whether USD/CHF would break through 0.8869 minor support, even before close.

In Europe, currently, FTSE is up 0.20%. DAX is up 0.73%. CAC is up 0.73%. Germany 10-year yield is up 0.0230 at -0.320. Earlier in Asia, Nikkei dropped -0.72%. Hong Kong HSI rose 0.16%. China Shanghai SSE rose 0.57%. Singapore Strait Times dropped -0.97%. Japan 10-year JGB yield rose 0.0120 to 0.106.

BoE Vlieghe: No further stimulus required if economy evolves as Feb central projections

BoE MPC member Gertjan Vlieghe said in a speech that “if the economy evolves broadly in line with our February central projection, then in my view it is likely that no further monetary stimulus is required… we will just complete the already announced QE programme”.

Though also, “given how low I think the neutral rate of interest is, there is no hurry at all to remove stimulus”, he added. “My preferred path for policy would be to keep the current monetary stimulus in place until well into 2023 or 2024, long enough to judge whether economic slack has indeed been eliminated fully, and inflation has returned to target sustainably, rather than being pushed up by temporary factors.”

UK PMI composite rose to 49.8, welcome signs of steadying

UK PMI Manufacturing rose to 54.9 in February, up from 54.1, above expectation of 54.0. PMI Services rose to 49.7, up from 39.5, above expectation of 40.5. PMI Composite rose to 49.8, up from 41.2.

Chris Williamson, Chief Business Economist at IHS Markit, said: “The UK economy showed welcome signs of steadying in February after the severe slump seen in January… In contrast, the manufacturing sector’s performance worsened amid escalating Brexit-related export losses and supply chain disruptions… More encouragingly, although the data hint at a renewed contraction of the economy in the first quarter, business expectations for the year ahead improved to the highest for almost seven years, suggesting the economy is poised for recovery. Confidence continued to be lifted by hopes that the vaccine roll-out will allow virus related restrictions to ease, outweighing concerns among many other firms of the potential further damaging impact of Brexit-related trading issues.”

UK retail sales dropped -8.2% mom in Jan, -5.5% below pre-pandemic level

UK retail sales dropped sharply by -8.2% mom in January, well below expectation of -1.0% mom. Ex-fuel sales dropped -8.8% mom, also way below expectation of -0.5% mom. All sectors saw a monthly decline in volume sales except for non-store retailers and food stores, who reported growth of 3.7% mom and 1.4% mom.

In the three months to January, retail sales dropped -4.9%, compared with the previous three months, with strong declines in both clothing stores and automotive fuel. Total sales volumes were at -5.5% below pre-pandemic level in February 2020.

Eurozone PMI manufacturing rose to 57.7 a 36-mth high, services dropped slightly to 44.7

Eurozone PMI Manufacturing rose to 57.7 in February, up from 54.8, well above expectation of 54.4. That’s also the highest level in 36 months. PMI Services dropped to 44.7, down from 45.4, slightly above expectation of 44.5. PMI Composite rose to 48.1, up from 47.8.

Chris Williamson, Chief Business Economist at IHS Markit said: “Ongoing COVID-19 lockdown measures dealt a further blow to the eurozone’s service sector in February, adding to the likelihood of GDP falling again in the first quarter. However, the impact was alleviated by a strengthening upturn in manufacturing, hinting at a far milder economic downturn than suffered in the first half of last year. Factory output grew at one of the strongest rates seen over the past three years, thanks to another impressive performance by German producers and signs of strengthening production trends across the rest of the region.

“Vaccine developments have meanwhile helped business confidence to revive, with firms across the eurozone becoming increasingly upbeat about recovery prospects. Assuming vaccine roll-outs can boost service sector growth alongside a sustained strong manufacturing sector, the second half of the year should see a robust recovery take hold.

“One concern is the further intensification of supply shortages, which have pushed raw material prices higher. Supply delays have risen to near-record levels, leading to near-decade high producer input cost inflation. At the moment, weak consumer demand – notably for services – is limiting overall price pressures, but it seems likely that inflation will pick up in coming months.”

Germany PMI Manufacturing surged to 60.6, up from 57.1, well above expectation of 56.5. That’s also the highest level in 36 months. PMI services, dropped to 45.9, down from 46.7, slightly below expectation of 46.5. PMI Composite rose to 51.3, up from 50.8, a 2-month high.

France PMI Manufacturing jumped to 55.0 in February, up from 51.6, well above expectation of 51.0. That’s also the highest reading in 3 years. PMI Services, however, dropped to 43.6, down from 47,3, well below expectation of 47.0. PMI Composite dropped further to 45.2, down from 47.7, a 3-month low.

Japan CPI core rose to -0.6% yoy in Jan, CPI core-core turned positive to 0.1% yoy

Japan CPI core (ex-food) climbed back to -0.6% yoy in January, up from -1.0% yoy, above expectation of -0.7% yoy. All item CPI also rose to -0.6% yoy, up from -1.2% yoy. CPI core-core (ex-food and energy) turned positive to 0.1% yoy, up from -0.4% yoy.

BoJ is set to review its monetary policy tools in March, to make the massive stimulus program “more sustainable and effective”. It’s reported that the central bank could replace some numerical guidelines for ETF purchases. A source to Reuters noted that “to make the BOJ’s policy sustainable, it needs to avoid buying too much ETFs when doing so is unnecessary”.

Japan PMI manufacturing rose to 50.6, but services dropped to 45.8

Japan PMI Manufacturing rose to 50.6 in February, up from 49.8, indicating a renewed improvement in the manufacturing sector. PMI Services, however, dropped to 45.8, down from 46.1. PMI Composite rose to 47.6, up from 47.1.

Usamah Bhatti, Economist at IHS Markit, said: “Latest flash PMI data signalled a further decline in business activity. New orders also fell solidly, led by weaker domestic demand. The latest data pointed to some brighter spots. New export orders stabilised… Employment levels expanded slightly… Input price inflation continued at a similar pace to January. Businesses were optimistic that business conditions would improve in the coming 12 months.

Australia PMI composite dropped to 54.4, strong employment, higher inflationary pressure supply chain disruption

Australia PMI Manufacturing dropped to 56.6 in February, down from 57.2. PMI Services dropped to 54.1, down from 55.6. PMI Composite dropped to 54.4, down from 55.9.

Andrew Harker, Economics Director at IHS Markit, said: “A key positive from the flash PMI data for Australia is the strongest pace of job creation since late-2018…. On a less positive note, growth in the economy has been accompanied by stronger inflationary pressures… Another factor potentially putting the brakes on growth, particularly in the manufacturing sector, is the ongoing disruption to supply chains amid global shipping problems which showed no sign of letting up.”

Australia retail sales rose 0.6% mom in Jan, NSW led the rise but Queensland dropped

Australia retail sales rose 0.6% mom in January, below expectation of 2.0% mom. All states and territories rose, except for Queensland. NSW led the rises, up 1.0%, as Greater Sydney saw COVID-19 restrictions eased in January. Queensland saw a fall of 1.5%, with COVID-19 restrictions in Brisbane leading to falls

Ben James, Director of Quarterly Economy Wide Surveys, said: “There continues to be variations in retail sales between states and territories, as COVID-19 restrictions are tightened or eased in different parts of the country.”

From New Zealand, PPI input slowed to 0.0% qoq in Q4, PPI output turned positive to 0.4% qoq.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.7726; (P) 0.7749; (R1) 0.7774; More…

AUD/USD surges to as high as 0.7861 so far, and the break of 0.7189 resistance confirms resumption of up trend from 0.5506. Intraday bias is back on the upside for 61.8% projection of 0.6991 to 0.7819 from 0.7563 at 0.8075. For now, outlook will remain bullish as long as 0.7730 support holds, even in case of retreat.

In the bigger picture, whole down trend from 1.1079 (2001 high) should have completed at 0.5506 (2020 low) already. Rise from 0.5506 could either be the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. But in any case, medium term rally is expected to continue as long as 0.7413 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q4 | 0.00% | 0.60% | ||

| 21:45 | NZD | PPI Output Q/Q Q4 | 0.40% | -0.30% | ||

| 22:00 | AUD | CBA Manufacturing PMI Feb P | 56.6 | 57.2 | ||

| 22:00 | AUD | CBA Services PMI Feb P | 54.1 | 55.6 | ||

| 23:30 | JPY | National CPI Core Y/Y Jan | -0.60% | -0.70% | -1.00% | |

| 0:01 | GBP | GfK Consumer Confidence Feb | -23 | -27 | -28 | |

| 0:30 | AUD | Retail Sales M/M Jan P | 0.60% | 2.00% | -4.10% | |

| 0:30 | JPY | Jibun Bank Manufacturing PMI Feb P | 50.6 | 49.7 | 49.8 | |

| 7:00 | EUR | Germany PPI M/M Jan | 1.40% | 0.70% | 0.80% | |

| 7:00 | EUR | Germany PPI Y/Y Jan | 0.90% | 0.20% | 0.20% | |

| 7:00 | GBP | Retail Sales M/M Jan | -8.20% | -1.00% | 0.30% | 0.40% |

| 7:00 | GBP | Retail Sales Y/Y Jan | -5.90% | 2.90% | 3.10% | |

| 7:00 | GBP | Retail Sales ex-Fuel M/M Jan | -8.80% | -0.50% | 0.40% | |

| 7:00 | GBP | Retail Sales ex-Fuel Y/Y Jan | -3.80% | 6.40% | 6.70% | |

| 7:00 | GBP | Public Sector Net Borrowing (GBP) Jan | 8.0B | 33.4B | ||

| 7:30 | CHF | Industrial Production Y/Y Q4 | -3.80% | -5.10% | ||

| 8:15 | EUR | France Manufacturing PMI Feb P | 55 | 51 | 51.6 | |

| 8:15 | EUR | France Services PMI Feb P | 43.6 | 47 | 47.3 | |

| 8:30 | EUR | Germany Manufacturing PMI Feb P | 60.6 | 56.5 | 57.1 | |

| 8:30 | EUR | Germany Services PMI Feb P | 45.9 | 46.5 | 46.7 | |

| 9:00 | EUR | Eurozone Manufacturing PMI Feb P | 57.7 | 54.4 | 54.8 | |

| 9:00 | EUR | Eurozone Services PMI Feb P | 44.7 | 44.5 | 45.4 | |

| 9:00 | EUR | Eurozone Current Account (EUR) Dec | 36.7B | 22.0B | 24.6B | |

| 9:30 | GBP | Manufacturing PMI Feb P | 54.9 | 54 | 54.1 | |

| 9:30 | GBP | Services PMI Feb P | 49.7 | 40.5 | 39.5 | |

| 13:30 | CAD | Retail Sales M/M Dec | 1.30% | |||

| 13:30 | CAD | Retail Sales ex Autos M/M Dec | 2.10% | |||

| 14:45 | USD | Manufacturing PMI Feb P | 58.5 | 59.2 | ||

| 14:45 | USD | Services PMI Feb P | 57.5 | 58.3 | ||

| 15:00 | USD | Existing Home Sales Jan | 6.56M | 6.76M | ||

| 15:00 | USD | Existing Home Sales Change M/M Jan | -2.70% | 0.70% |