Canadian Dollar rises broadly in early US session, with the help from better than expected GDP data. Euro is also firmer on German and French GDP data. While markets are back in risk-off mode, Yen, and to a lesser extent Dollar and Swiss Franc, turn softer. As for the week, Sterling and Kiwi are currently the strongest, while Yen and Aussie are the weakest.

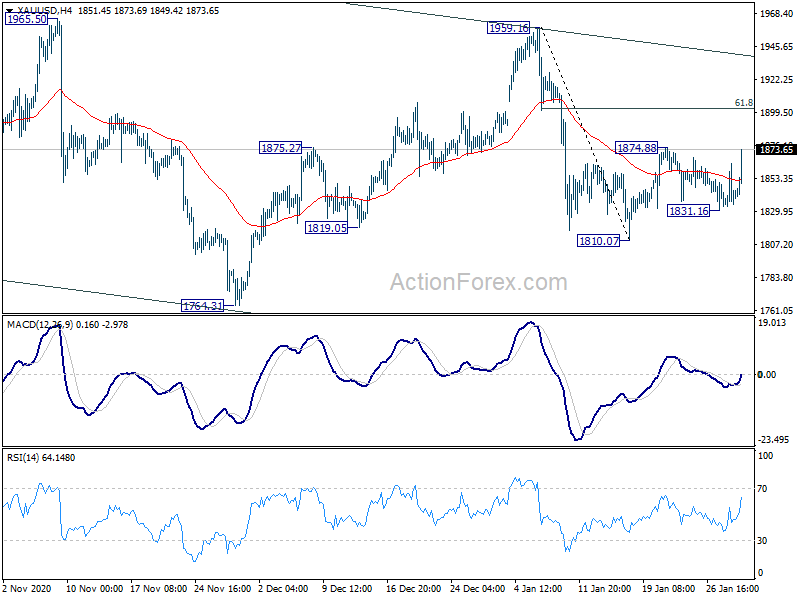

Technically, Gold would be a focus before weekly close. Today’s rise argues that rebound from 1810.07 might be resuming. Break of 1874.88 would confirm and could hint on Dollar weakness elsewhere. Though, as such rise is seen as a corrective move, upside should be limited by 61.8% retracement of 1959.16 to 1810.07 at 1902.02.

In Europe, currently, FTSE is down -1.66%. DAX is down -1.19%. CAC is down -1.34%. Germany 10-year yield is up 0.0417 at -0.496. Earlier in Asia, Nikkei dropped -1.89%. Hong Kong HSI dropped -0.94%. China Shanghai SSE dropped -0.63%. Singapore Strait Times dropped -0.61%.

US personal income rose 0.6% mom in Dec, spending dropped -0.2% mom

US personal income rose 0.6% mom, or USD 116.6B in December, well above expectation of 0.1% mom. Spending dropped -0.2% mom, or USD -27.9B, versus expectation of -0.40% mom. Headline PCE pride index accelerated to 1.3% yoy. Core PCE price index accelerated to 1.5% yoy.

Employment cost index rose 0.7% in Q4, above expectation of 0.5%.

Canada GDP grew 0.7% mom in Nov, above expectations

Canada GDP grew 0.7% mom in November, above expectation of 0.4% mom. This is the seventh consecutive monthly gain. Total economic activity was still around -3% below the pre-pandemic level in February. Good-producing industries grew 1.2% mom while services-producing industries rose 0.5% mom. 14 of 20 industrial sectors posted gains. Meanwhile, preliminary information indicates an approximate 0.3% mom GDP growth in December.

Also released, Canada IPPI rose 1.5% mom in December versus expectation of 1.4% mom. RMPI rose 3.5% mom versus expectation of 2.5% mom.

German GDP grew 0.1% qoq in Q4, down -5% for whole 2020

Germany GDP grew 0.1% qoq in Q4, above expectation of 0.0% qoq. DeStatis said in Q4, “the recovery process slowed due to the second coronavirus wave and another lockdown imposed at the end of the year. This affected household consumption in particular, while exports of goods and gross fixed capital formation in construction supported the economy. ” For the year 2020 as a whole, GDP dropped -5.0%.

Also from Germany, unemployment dropped -41k in December versus expectation of 7k rise. Unemployment rate was unchanged at 6.0%. Import price index rose 0.6% mom in December, versus expectation of 1.0% mom.

France GDP dropped -1.3% qoq in Q4 on lockdown and curfews

France GDP contracted -1.3% qoq in Q4, better than expectation of -3.9% qoq. GDP was -5% below its level a year ago. Insee said that “the loss of activity this quarter was marked by the lockdown in effect from the end of October to mid-December and by the curfews put in place during the months of October and December”. Over the full 2020, GDP dropped -8.3%.

Looking at some details, household consumption dropped -5.4%. Gross fixed capital formation grew 2.4%. Total domestic demand dropped -2.7%. Exports 4.8%, more than imports’s 1.3%. Foreign trade made a positive contribution to GDP growth, added 0.9%. Change in inventories also made a positive contribution by 0.4%.

Swiss KOF dropped to 96.5, gloomy economic prospects at beginning of the year

Swiss KOF Economic Barometer dropped to 96.5 in January, down from 104.1, missed expectation of 101.5, and back below long-term average of 100. KOF said, “after reaching an interim pandemic high in September, COVID-19 is now weighing more heavily on the economy again. The pandemic is causing gloomy economic prospects at the beginning of the year.”

“Responsible for the decline are in particular the indicator bundles for accommodation and food service activities as well as other services,” KOF added. “But the outlook for manufacturing, financial and insurance services and private consumer demand is also less favourable than before. The outlook for construction is stable and foreign demand could provide a stronger impulse.”

BoJ Opinions: Downward pressure strong but moderate improving trend maintained

In the Summary of Opinions at BoJ’s January 20-21 meeting, it’s noted, “the impact of the reinstatement of the state of emergency for 11 prefectures… should be monitored carefully given that private consumption in these prefectures accounts for nearly 60 percent of Japan’s.”While downward pressure is “likely to be strong for the time being”, the economy is expected to “maintain its moderate improving trend”.

BoJ also noted, “this year, it is necessary to closely monitor the broad impact of political developments overseas, such as the change of government in the United States and the replacement of the Chancellor of Germany, on economic activities and financial conditions at home and abroad.”

On monetary policy, one member said, “in terms of yield curve control and purchases of assets such as exchange-traded funds (ETFs), it is crucial for the Bank to conduct them more flexibly in a prioritized manner while maintaining the current policy framework.”

Japan industrial production dropped -1.6% mom in Dec, but rebound expected in Jan

Japan industrial production dropped -1.6% mom in December, below expectation of -1.5% mom. Though, on the bright side, manufacturers surveyed by the Ministry of Economy, Trade and Industry (METI) expected output to rebound 8.9% in January and decline 0.3% in February. The government also maintained that industrial production was picking up.

Also from Japan, unemployment rate was unchanged at 2.9% in December, better than expectation of a tick up to 3.0%. Housing starts dropped -9.0% yoy in December versus expectation of -4.9% yoy. Consumer confidence dropped to 29.6 in January, down from 31.8, above expectation of 28.1. Tokyo CPI core improved to -0.4% yoy in January, up from -0.9% yoy, above expectation of -0.6% yoy.

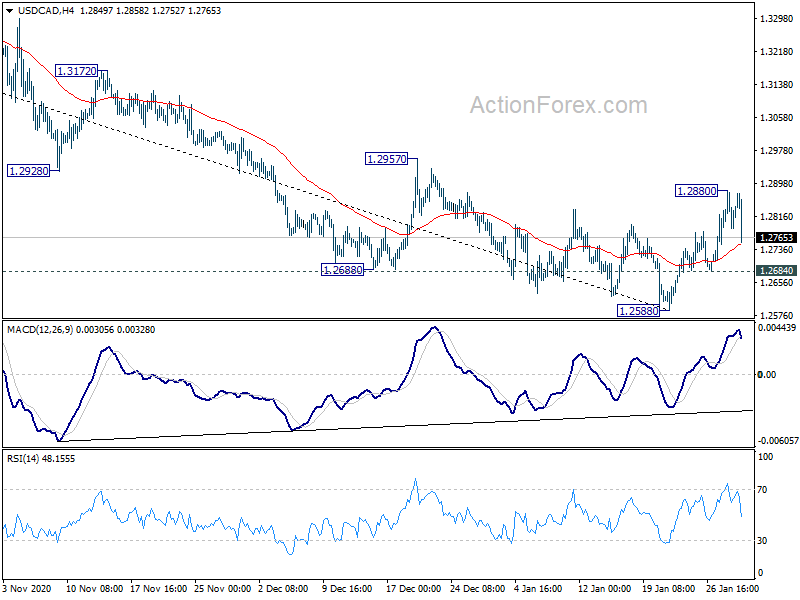

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2784; (P) 1.2833; (R1) 1.2878; More….

Intraday bias in USD/CAD is turned neutral with current steep retreat. Though, further rise is still expected as long as 1.2684 minor support holds. Break of 1.2880 will extend the rebound from 1.2588 short term bottom to 1.2957/94 resistance zone next. However, break of 1.2684 minor support will argue that the rebound has completed and bring retest of 1.2588 low.

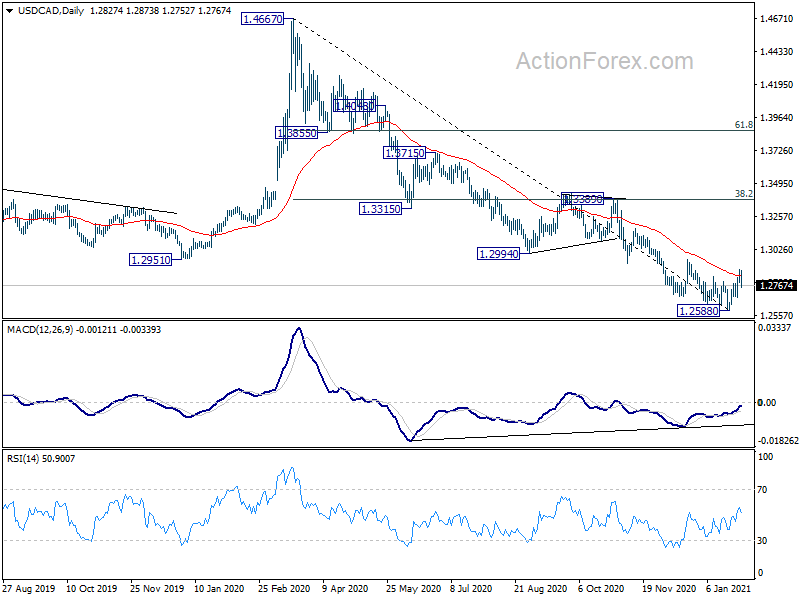

In the bigger picture, fall from 1.4667 is seen as the third leg of the corrective pattern from 1.4689 (2016 high). Further decline should be seen back to 1.2061 (2017 low). In any case, break of 1.3389 resistance is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Jan | -0.40% | -0.60% | -0.90% | |

| 23:30 | JPY | Unemployment Rate Dec | 2.90% | 3.00% | 2.90% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Dec P | -1.60% | -1.50% | -0.50% | |

| 23:50 | JPY | Industrial Production Y/Y Dec P | -3.20% | -3.90% | ||

| 00:30 | AUD | Private Sector Credit M/M Dec | 0.30% | 0.20% | 0.10% | |

| 00:30 | AUD | PPI Q/Q Q4 | 0.50% | 0.40% | ||

| 00:30 | AUD | PPI Y/Y Q4 | -0.10% | -0.40% | ||

| 05:00 | JPY | Housing Starts Y/Y Dec | -9.00% | -4.90% | -3.70% | |

| 05:00 | JPY | Consumer Confidence Index Jan | 29.6 | 28.1 | 31.8 | |

| 06:30 | EUR | France Consumer Spending M/M Dec | 23.00% | 15.50% | -18.90% | -18.00% |

| 06:30 | EUR | France GDP Q/Q Q4 P | -1.30% | -3.90% | 18.70% | |

| 07:00 | EUR | Germany Import Price Index M/M Dec | 0.60% | 1.00% | 0.50% | |

| 07:00 | EUR | Germany Import Price Index Y/Y Dec | -3.40% | -3.20% | -3.80% | |

| 08:00 | CHF | KOF Leading Indicator Jan | 96.5 | 101.5 | 104.3 | |

| 08:55 | EUR | Germany Unemployment Change Dec | -41K | 7K | -37K | -40K |

| 08:55 | EUR | Germany Unemployment Rate Dec | 6.00% | 6.10% | 6.10% | 6.00% |

| 09:00 | EUR | Germany GDP Q/Q Q4 P | 0.10% | 0.00% | 8.50% | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Dec | 12.30% | 11.20% | 11.00% | |

| 13:30 | CAD | GDP M/M Nov | 0.70% | 0.40% | 0.40% | |

| 13:30 | CAD | Industrial Product Price M/M Dec | 1.50% | 1.40% | -0.60% | |

| 13:30 | CAD | Raw Material Price Index Dec | 3.50% | 2.50% | 0.60% | |

| 13:30 | USD | Personal Income Dec | 0.60% | 0.10% | -1.10% | -1.70% |

| 13:30 | USD | Personal Spending Dec | -0.20% | -0.40% | -0.40% | -0.70% |

| 13:30 | USD | PCE Price Index M/M Dec | 0.40% | 0.00% | ||

| 13:30 | USD | PCE Price Index Y/Y Dec | 1.30% | 1.10% | ||

| 13:30 | USD | Core PCE Price Index M/M Dec | 0.30% | 0.10% | 0.00% | |

| 13:30 | USD | Core PCE Price Index Y/Y Dec | 1.50% | 1.30% | 1.40% | |

| 13:30 | USD | Employment Cost Index Q4 | 0.70% | 0.50% | 0.50% | |

| 14:45 | USD | Chicago PMI Jan | 58 | 58.7 | ||

| 15:00 | USD | Pending Home Sales M/M Dec | -1.20% | -2.60% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan F | 79.2 | 79.2 |

RULE-BASED Pocket Option Strategy That Actually Works | Live Trading

RULE-BASED Pocket Option Strategy That Actually Works | Live Trading This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)