It’s the same old story as Asian markets open in risk-on mode. Commodity currencies strengthen broadly, but led by New Zealand Dollar this time. On the other hand, Swiss Franc, Yen and Dollar are the weaker ones, while Euro and Sterling are mixed. Trading could be subdued today with a thin economic calendar. ECB President Christine Lagarde would speak but she’s unlikely to say something different from what she said last week. Though, German Ifo business climate might trigger some reactions.

Technically, Euro would be a focus after last week’s late rebound. Levels to watch include 0.8923 minor resistance in EUR/GBP, 1.0790 minor resistance in EUR/CHF and 1.5830 minor resistance in EUR/AUD. Firm break of these levels would be needed to confirm underlying momentum for a sustainable rebound. Otherwise, selloff in Euro could come back later in the week.

In Asia, currently, Nikkei is up 0.43%. Hong Kong HSI is up 2.03%. China Shanghai SSE is up 0.56%. Singapore Strait Times is down -0.28%. Japan 10-year JGB yield is down -0.0052 at 0.037.

Australia goods exports jumped 16% in Dec, imports dropped -9%

According to preliminary data, Australia’s export of goods rose 16% mom to AUD 34.9B. Imports of goods dropped -9% mom to AUD 26.0B. There was a goods trade surplus of AUD 9.0B.

Exports to China jumped 21% to AUD 2312m, to Japan rose 24% to AUD 864m, to US rose 58% to AUSD 678m, to India rose 35% to AUD 339m, to South Korea dropped -14% to AUD 317m.

Imports from China dropped -7% to AUD 641m, from US dropped -33% to AUD 1274m, from Germany dropped -10% to AUD 127m, from Japan rose 6% to 95m, from Thailand rose 8% to AUD 101m.

“Imports have fallen following a November spike to be more in line with recent history”, said ABS Head of International Statistics, Katie Hutt, “while exports of metalliferous ores and cereals are the strongest in history, resulting in the fourth highest goods trade surplus on record”.

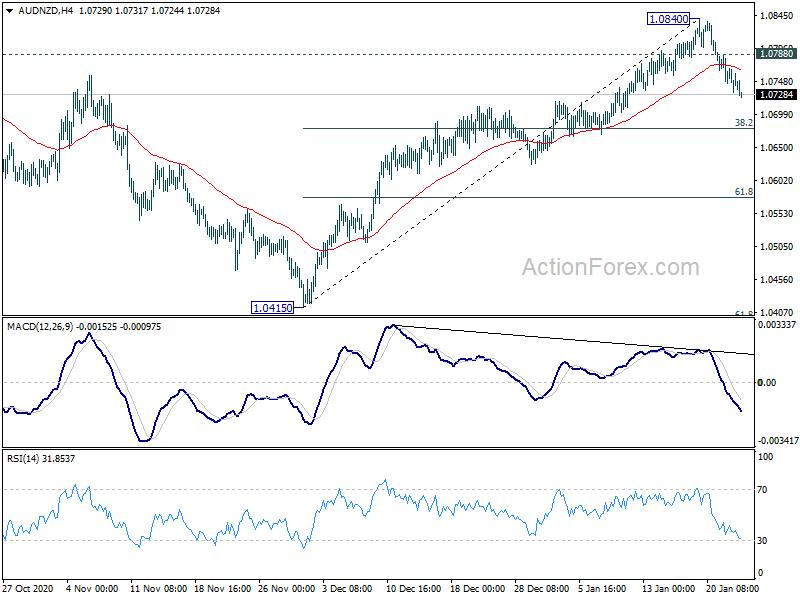

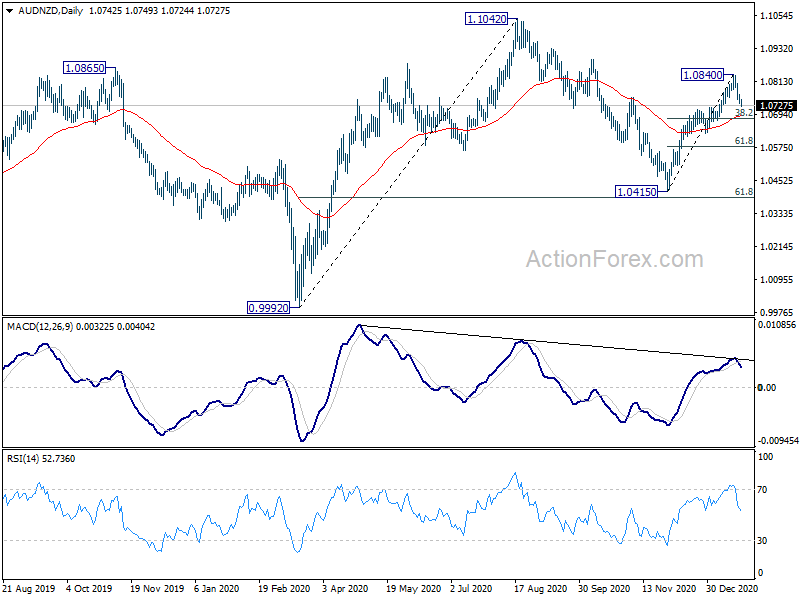

AUD/NZD in correction downwards, but no change in bullish trend

AUD/NZD formed a short term top at 1.0840 on overbought condition and turn into corrective fall. While some more downside is likely in the cross, we’re not expecting a complete reversal in fortune. Downside of pull back should be contained by 38.2% retracement of 1.0415 to 1.0840 at 1.0678, which is close to 55 day EMA (now at 1.0688). Above 1.0788 minor resistance will bring retest of 1.0840 resistance first.

However, firm break of 1.0678 would bring deeper fall to 61.8% retracement at 1.0577. Overall, the depth of the correction could eventually determine how far the rise from 1.0415 would extend to.

The Week ahead: Fed to stand pat with wait-and-see approach

FOMC is widely expected to stand pat this week and adopt a wait-and-see approach. Overall tone regarding economic outlook should remain cautious for the short term and upbeat for the medium term, depending on vaccine roll-outs and the impact on coronavirus infections. While Chair Jerome Powell would be pressed on topics like tapering, he would most certainly remain non-committal to any plan of scaling back the asset purchases. After, Fed is clear to allow moderate inflation overshoot ahead to make up for the persistent misses. There is no sign of achieving that yet. On the central bank front, BoJ will release minutes and summary of opinions.

Suggested reading on Fed: FOMC Preview – Cautious about Economic Weakness but Fiscal Stimulus should lend Support

On the data front, we’d maintain that forward looking and sentiment indicators are the more important ones. Those include US consumer confidence, Germany Ifo business climates, Swiss KOF economic barometer and Australia NAB business confidence. Meanwhile, GDP from US, France and Canada will also be released. Here are some highlights for the week:

- Monday: Germany Ifo business climate.

- Tuesday: BoJ minutes, corporate services price index; UK employment; US house price indices, consumer confidence.

- Wednesday: Australia CPI, NAB business confidence; Germany Gfk consumer sentiment; US durable goods orders, FOMC rate decision.

- Thursday: New Zealand trade balance, Australian import prices; Japan retail sales; Swiss trade balance; Germany CPI; Canada building permits; US GDP, jobless claims, trade balance, new home sales, leading indicators.

- Friday: Japan Tokyo CPI, BoJ summary of opinions, industrial production, consumer confidence, housing starts. Australia PPI, private sector credit; France GDP; Germany import prices, unemployment; Eurozone M3 money supply; Swiss KOF economic barometer; Canada GDP, IPPI and RMPI; US personal income and spending, employment cost index, Chicago PMI, pending home sales.

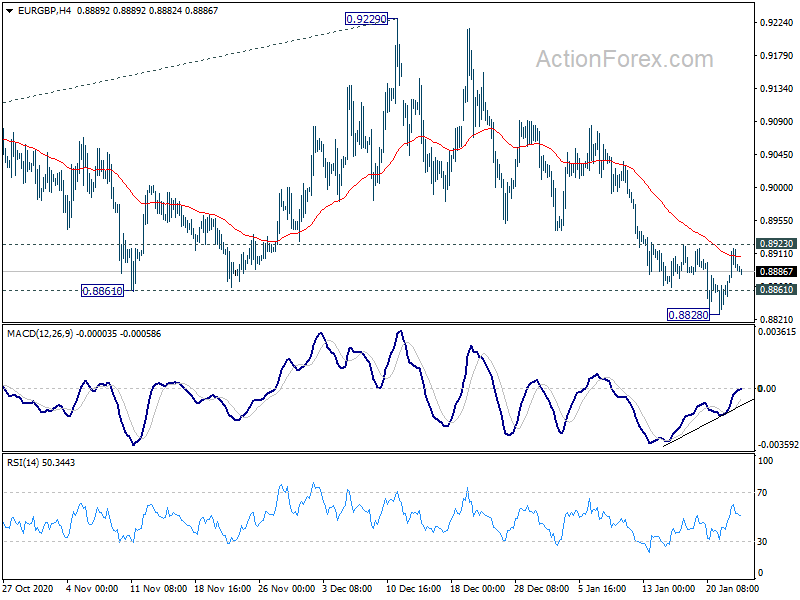

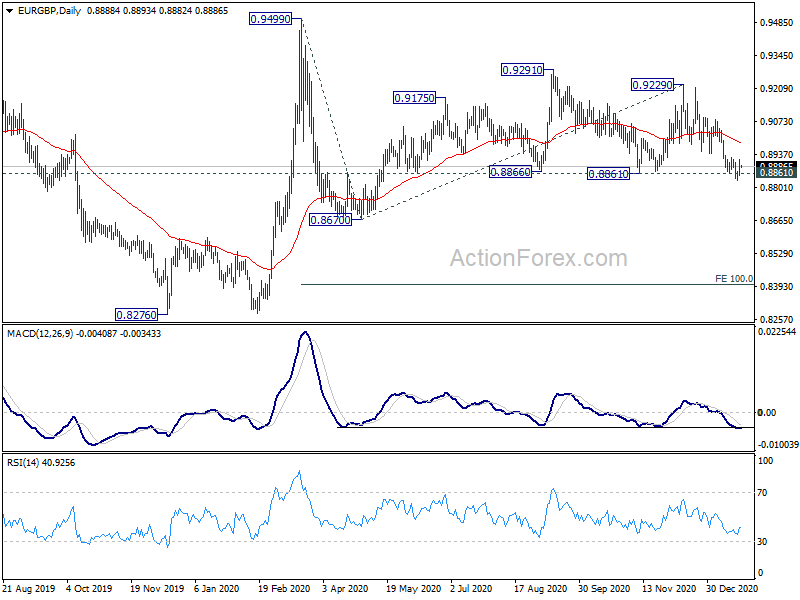

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8863; (P) 0.8890; (R1) 0.8923; More…

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, firm break of 0.8828, and sustained trading below 0.8861 will target 0.8670 support, as the third leg of pattern from 0.9499. On the upside, though, break of 0.8923 resistance will confirm defense of 0.8861. Intraday bias will be turned back to the upside for 55 day EMA (now at 0.8983) first.

In the bigger picture, we’re seeing the price actions from 0.9499 as developing into a corrective pattern. That is, up trend from 0.6935 (2015 low) would resume at a later stage. This will remain the favored case as long as 0.8276 support holds. Decisive break of 0.9499 will target 0.9799 (2008 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:00 | EUR | Germany IFO Business Climate Jan | 92.0 | 92.1 | ||

| 09:00 | EUR | Germany IFO Current Assessment Jan | 90.7 | 91.3 | ||

| 09:00 | EUR | Germany IFO Expectations Jan | 93.2 | 92.8 |