Yen had a U-turn today and breaks near term support level against Dollar. Resilience in treasury yield is seen as a factor for Yen’s weakness. After a brief set back yesterday, US 10-year yield looks set to extend recent rally through 0.78 handle. German 10-year yield is also trying to regain -0.5 handle too. Stock markets are relatively steady, with mixed European indices. DOW futures point to mild gain but it’s unsure whether it could reclaim 28000 handle. Staying in the currency markets, Euro and Swiss Franc are still the strongest for the week. New Zealand Dollar and Yen are now the weakest, followed by Sterling. Dollar is mixed, awaiting FOMC minutes for some guidance.

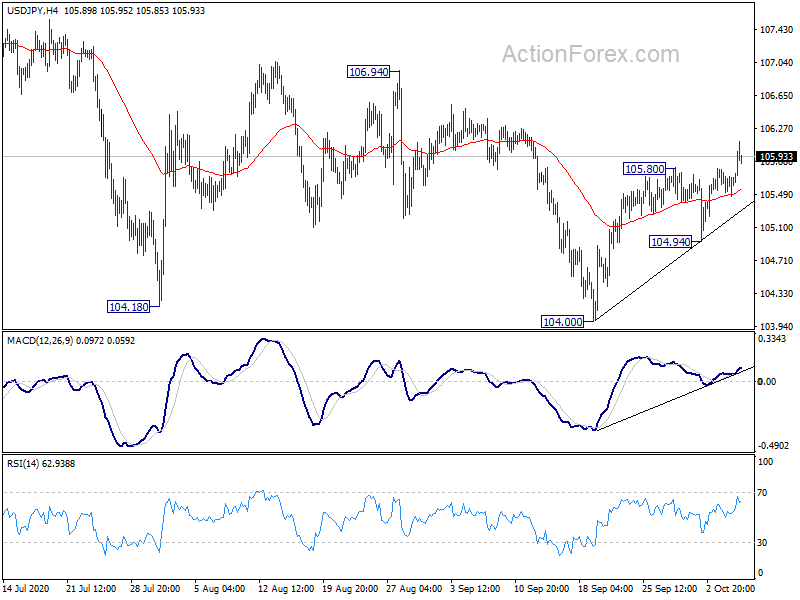

Technically, the risk of selloff in Yen crosses is eased for now. The first focus is on whether USD/JPY could extend the rebound from 104.00 to 106.94 key near term resistance. Then, second focus is whether such move would prompt stronger rebound in Yen crosses in general, or translate into Dollar strength elsewhere. Or, say, rise in USD/JPY and EUR/JPY would keep EUR/USD in range below 1.1807, just like what USD/JPY did below 105.80 a while ago.

In Europe, currently, FTSE is up 0.18%. DAX is down -0.35%. CAC is down -0.12%. German 10-year yield is up 0.0128 at -0.494. Earlier in Asia, Nikkei dropped -0.05%. Hong Kong HSI rose 1.09%. Singapore Strait Times rose 0.36%. Japan 10-year JGB yield rose 0.0049 to 0.042. China remained on holiday.

– advertisement –

ECB Lagarde: Pandemic crisis might leave behind more pronounced divergences in Eurozone

In a written interview with Harvard International Review, ECB President Christine Lagarde said the pandemic is a “common global shock” but the “local impact is going to be uneven”. Output losses in H1 ranged from less than -11.5% in Germany to more than -22.7% in Spain. These differences “reflect both the severity of the outbreak, the design of the national response – itself a function of diverse fiscal positions –, the economic structure, the sectoral activity, the fiscal absorption capacity and the resilience of the corporate and financial sectors.”

“It is clear that the crisis might leave behind a legacy of even more pronounced divergences among the economies of the euro area than we have observed so far. Countries will return to pre-COVID GDP levels at different points in time, some earlier, some later. Those countries set to struggle for longer with the aftermath of the pandemic shock will likely suffer from deeper and longer-lasting scars. All this risks prolonging and even entrenching structural heterogeneity within the euro area.” She added.

That’s the reason why the Next Generation EU recovery package is “so critical. It has a “dual function”, supporting depend and increase the structural resilience and growth potential of the “entire area”.

BoE Tenreyro: Productivity gain from WFH trend and online shopping

BoE policymaker Silvana Tenreyro said “work-from-home trend” could bring productivity gains in the medium term. Also, shift to online shopping could bring productivity gain too.

For Europe, US and the UK, the risk is that “we undershoot inflation targets. Also, she warned, the the full recovery from the pandemic could be hindered by stretched budgets of governments around the world..

UK Truss: We very clearly wants a Canada style deal with EU

UK Trade Secretary Liz Truss told LBC that the UK was “very clear” about the deal they want with the EU. That is a “Canada style deal where we control our own rules and regulations, we are not subject to the European court and we get a good deal on fisheries.”

“There’s a deal there to be done and I think it makes sense for the EU and the UK to sign that deal. But what I’m doing as trade secretary is making sure we’ve got options,” she added. “So we are working on a deal with the United States, we’re working on a deal with the trans-pacific partnership, because what I want is for British exporters to have lots of markets where they can send our fantastic products.”

Separately, Prime Minister Boris Johnson told the parliament, “this country has not only left the European Union but on January 1 we will take back full control of our money, our borders and our laws.”

Data from Eurozone painted a mixed picture

Economic data from Eurozone painted a mixed picture. Italy retail sales rose sharply by 8.2% mom in August, much stronger than expectation of 3.8% mom rise. Germany industrial production, on the other hand, dropped -0.2% mom in August, below expectation of 1.5% mom. France trade deficit widened to EUR -7.7B in August, versus expectation of EUR -6.5B. Also release, Swiss foreign currency reserves rose to CHF 874B in September, up form CHF 849B.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.48; (P) 105.63; (R1) 105.80; More...

Intraday bias in USD/JPY remains on the upside at this point, for 106.94 resistance. Current development argues revives the case that down trend from 111.71 has completed on bullish convergence condition in daily MACD. On the upside, break of 106.94 resistance will confirm and turn outlook bullish. On downside, break of 104.94 support is needed to indicate completion of the rebound. Otherwise, further rise will remain mildly in favor in case of retreat.

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. However, sustained break of 112.22 resistance should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Sep | 36.2 | 42.5 | ||

| 5:00 | JPY | Leading Economic Index Aug P | 88.8 | 89.4 | 86.9 | 86.7 |

| 6:00 | EUR | Germany Industrial Production M/M Aug | -0.20% | 1.50% | 1.20% | 1.40% |

| 6:45 | EUR | France Trade Balance (EUR) Aug | -7.7B | -6.5B | -7.0B | |

| 7:00 | CHF | Foreign Currency Reserves (CHF) Sep | 874B | 848B | 849B | |

| 8:00 | EUR | Italy Retail Sales M/M Aug | 8.20% | 3.80% | -2.20% | |

| 14:00 | CAD | Ivey PMI Sep | 67.8 | |||

| 14:30 | USD | Crude Oil Inventories | -2.0M | |||

| 18:00 | USD | FOMC Minutes |