Sterling remains the weakest one for the week, without a doubt in the otherwise mixed forex markets. Overall risk sentiments stabilized with the overnight rebound in US stocks. Dollar has pared back much of this week’s gains together with Yen. Euro is currently the stronger one for today, as helped by cross buying against the Pound, and the recovery against Dollar and Yen. Yet, the common currency will remain vulnerable to another decline, subject to ECB’s comments on its recent strength.

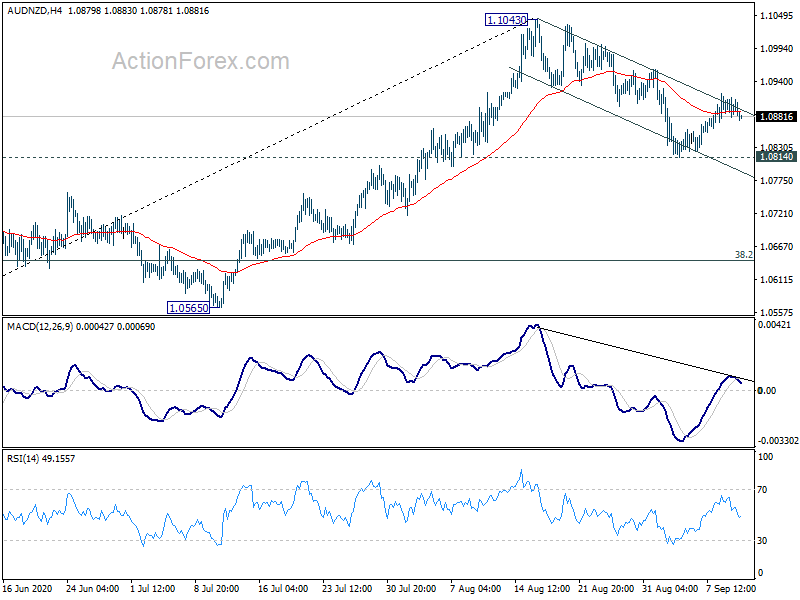

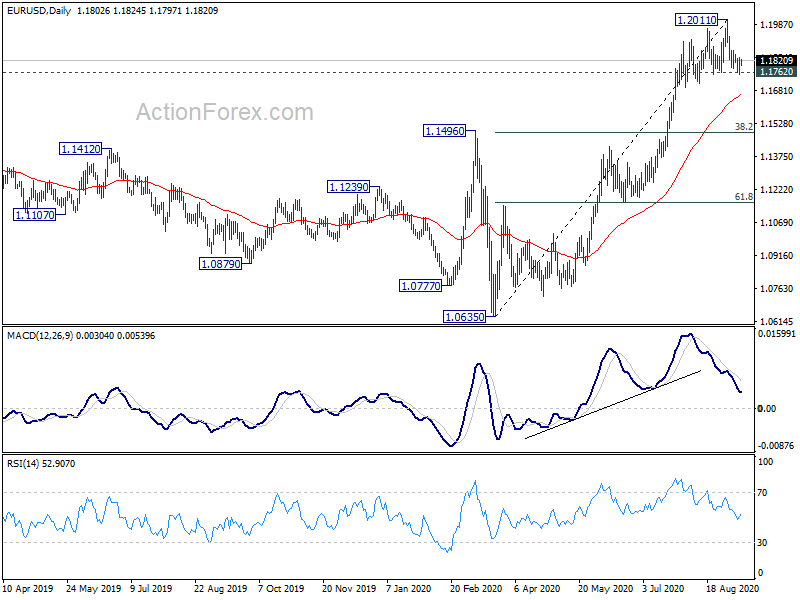

Technically, considering ECB risks, 1.1762 support in EUR/USD and 124.44 support in EUR/JPY would be the focuses for today. The eventual reactions to ECB as well as these two support levels could define the near term direction for next few weeks. AUD/NZD is another one to watch as it appears to have completed a recovery after hitting near term channel resistance. Renewed selling could drag the Aussie down elsewhere.

– advertisement –

In Asia, currently, Nikkei is up 0.69%. Hong Kong HSI is up 0.01%. China Shanghai SSE is down -0.06%. Singapore Strait Times is down -0.37%. Japan 10-year JGB yield is down -0.0049 at 0.025. Overnight, DOW rose 1.6%. S&P 500 rose 2.01%. NASDAQ rose 2.71%. 10-year yield rose 0.019 to 0.703.

Euro resilient as ECB comments on its strength awaited

ECB meeting is a major focus today and no policy change is expected. ECB should maintain the deposit rate at -0.5%. The main refi rate and the marginal lending rate will also stay unchanged at 0% and 0.25% respectively. The PEPP program will continue to run with a total envelope of 1.35 trillion euro. We expect the central bank will reiterate the guidance that the purchases “will” continue “until at least the end of June 2021 and, in any case, until the Governing Council judges that the coronavirus crisis phase is over”.

Attention will main be on ECB’s view on recent Euro strength, against Dollar mainly. Chief Economist Philip Lane’s speech at Jackson Hole. Lane raised concerns that rising EURUSD could prolong weak inflation and inflation expectations. As he suggested, “we have an inflation mandate and we care about the overall performance of the European economy”. He added that there has been “a repricing in recent weeks” in EURUSD “to some degree”.

EUR/USD has been resiliently holing on to 1.1762 near term structure support recently. But traders might only be waiting for ECB Governor Christine Lagarde’s nod on selling it through the support to correct the strong rally since March.

Some suggested readings on ECB:

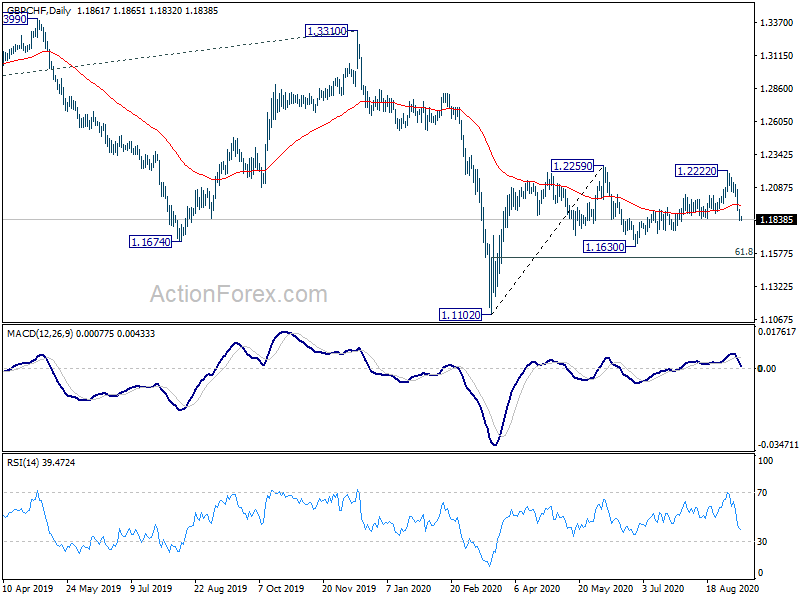

GBP/CHF targeting 1.1630, awaits extraordinary Brexit meeting

Sterling remains the worst performer for the week on concerns over Brexit uncertainties. It’s reported that EU is considering legal against the UK According to a draft working paper by the EU, UK’s Internal Market Bill is seen as a “clear breach of substantive provisions” of the Brexit withdrawal agreement

European Commission Vice-President Maroš Šefčovič will travel to London today to meet UK Chancellor of the Duchy of Lancaster Michael Gove for an ” extraordinary meeting of the Joint Committee” that oversees Brexit implementation. The EU said it “seeks clarifications from the UK on the full and timely implementation of the Withdrawal Agreement” EU’s chief negotiator Michel Barnier, arrived in London yesterday, is expected to confront the UK counterpart David Frost over the issue too.

GBP/CHF’s decline from 1.222 extends to as low as 1.1831 so far. Such decline is currently seen as the third leg of the consolidation pattern from 1.2259. Deeper fall could be seen to 1.1630 and probably below. But strong support is expected at 61.8% retracement of 1.1102 to 1.2259 at 1.1544 to contain downside and bring rebound.

However, note that GBP/CHF was just rejected by 55 week EMA. Sustained break of 1.1544 would in turn argue that larger down trend is indeed resume for a new low below 1.1102.

BoC left interest rate and QE program unchanged

Overnight, BOC announced to leave the policy rate at the effective lower bound of 0.25% and maintain the pace of asset purchases at CAD 5B/week of Canadian government bonds. While acknowledging that economic activities have rebounded more than expected since the July meeting, the members remained cautious about the outlook, especially on subdued inflation.

On the monetary policy outlook, BOC reiterated to “hold the policy interest rate at the effective lower bound until economic slack is absorbed so that the 2% inflation target is sustainably achieved”. More in BOC Left Policy Rate and QE Unchanged, Pledged to Calibrate Measures when Needed.

On the data front

Japan machine orders rose 6.3% mom in July, well above expectation of 1.9% mom. Australia consumer inflation expectations slowed to 3.1% in September. UK RICS housing price balance jumped to 44 in August. France and Italy will release industrial production. US will release PPI and jobless claims.

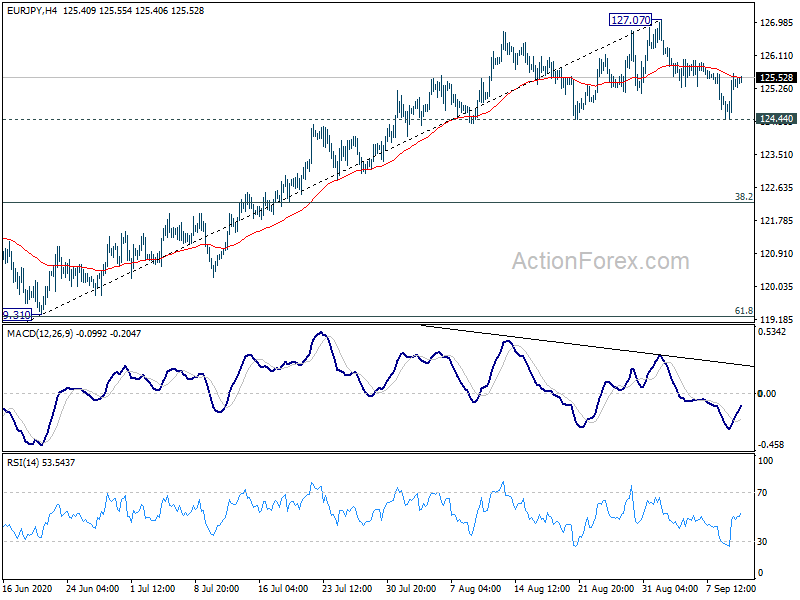

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.64; (P) 125.14; (R1) 125.86; More….

With 124.44 support intact, intraday bias in EUR/JPY remains neutral first. Larger rise is in favor to continue and break of 127.07 will resume the rally from 114.42, to 128.67 fibonacci level. Nevertheless, considering bearish divergence condition in daily MACD, firm break of 124.44 will confirm short term topping. Intraday bias will be turned back to the downside for 55 day EMA (now at 124.01) and further to 38.2% retracement of 114.42 to 127.07 at 122.23.

In the bigger picture, whole down trend from 137.49 (2018 high) could have completed at 114.42 already. Rise from 114.42 would target 61.8% retracement of 137.49 to 114.42 at 128.67 next. Sustained break there will pave the way to 137.49 (2018 high). This will remain the preferred case for now, as long as 119.31 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Aug | 44% | 25% | 12% | |

| 23:50 | JPY | Machinery Orders M/M Jul | 6.30% | 1.90% | -7.60% | |

| 1:00 | AUD | Consumer Inflation Expectations Sep | 3.10% | 3.30% | ||

| 6:45 | EUR | France Industrial Output M/M Jul | 5.10% | 12.70% | ||

| 8:00 | EUR | Italy Industrial Output M/M Jul | 4.00% | 8.20% | ||

| 11:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | ||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | USD | PPI M/M Aug | 0.20% | 0.60% | ||

| 12:30 | USD | PPI Y/Y Aug | -0.70% | -0.40% | ||

| 12:30 | USD | PPI Core M/M Aug | 0.20% | 0.50% | ||

| 12:30 | USD | PPI Core Y/Y Aug | 0.30% | 0.30% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 4) | 838K | 881K | ||

| 14:00 | USD | Wholesale Inventories Jul F | -0.10% | -0.10% | ||

| 14:30 | USD | Natural Gas Storage | 35B | |||

| 15:00 | USD | Crude Oil Inventories | -9.4M |